🎢Cannabis Earnings Review: Canadian LPs

A look at MRQ for the Top 5 Canadian LPs: Canopy (CGC), Aurora (ACB), Cronos (CRON), Aphria (APHA), and Tilray (TLRY)

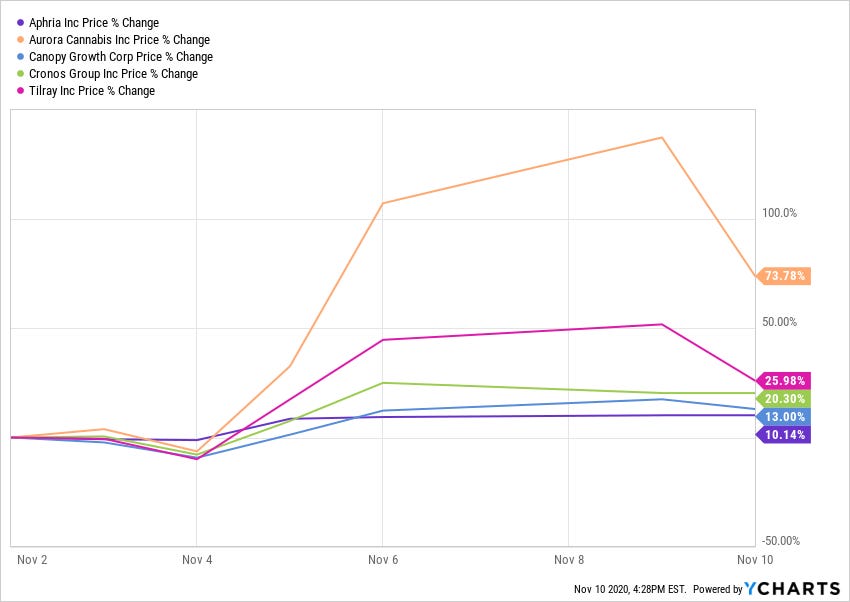

Overall, numbers from CGC, ACB, CRON, TLRY, and APHA are less than impressive. Although the market cap. for these companies have undergone some correction from the high flying days of Summer/Fall 2018, there’s still more work to be done to establish these companies as long-term investments rather than short-term trades (as seen by huge increase since election day to today’s dip). A closer look at these 5 companies show that while numbers matter a little, market size/cash/opportunity matter a lot more. The recent increase in publicly traded Cannabis names is largely overdone (with significant uncertainty and unknowns still present) and as I mentioned Sunday, a large swing to the downside / roller coaster ride is expected). It also seems like companies are trading as if U.S. federal legalization is happening in the next 2 years (2-4 years more likely).

Summary:

Valuation / Analyst Estimates not a factor. HOLD or SELL ratings don’t seem to be impacting valuations. The top 5 LPs are currently trading at 9.3x EV/Revenue (2021E) and 5.8x EV/Revenue (2022E) — only APHA and ACB are expected to be EBITDA+ for 2021E. There is definitely a premium applied to the top 5 LPs (especially those that are closer to EBITDA+) vs smaller/fragmented LPs.

Revenue lags MSOs / Growth seems low. Several MSOs (Curaleaf, GTI, Trulieve) are in the $100M+ quarterly revenue club (Cresco Labs is close) while only one Canadian LP (CGC) approach that today. CGC grew 23% Q/Q. ACB flat Q/Q. APHA slightly down Q/Q at (4%). TLRAY essentially flat Q/Q (4%). CRON up 10% Q/Q but on a very small base (~$10M revenue last Q).

Low Gross Margins (GM) for 3/5 LPs. Positive GM not a given, CRON actually has negative GMs, CGC ~19% GM and TLRY ~7% GM. APHA ~52% GM and ACB ~48% GM makes both best-in-class by a lot vs. Peers.

EBITDA. Canadian LPs are further away than MSOs when it comes to turning EBITDA positive. Even at year-end 2022E, CGC doesn’t project to be EBITDA+.

Cash. Canadian LPs seem to have easier access to ATM and deep-pocketed partners (CGC/Constellation and CRON/Altria). The ability to sustain high burn rates through cash seems more important than revenue/revenue growth in the near-term.

Media. The ability to get on CNBC or other major media outlets to drum up investors interest matter (correlation between premium multiples/CNBC appearances? — APHA, CGC, ACB on CNBC/Mad Money often)

Do write-offs, strategy/focus, and dilution matter? Overspending on CapEx (greenhouses), write-offs, and funding through ATMs don’t seem to be too concerning right now — seems like most are betting on a $10B+ market cap winner emerging and spreading bets across a few LPs.

Canopy Growth (CGS) — Q2/FY21 (reported 11/9):

🤯 GM at ~19%, up from ~7% GM Q/Q due to lower production output and underutilized assets

💰 C$135.3M, up 23% Q/Q, 19% GM (up from 14% Q/Q). Net loss of C$96.6M, a $339.2M wider loss Q/Q

🔥 Steep loss of ($85.7M) EBITDA, an improvement vs. ($150.4M) Q/Q

🩸 (C$190.4M) FCF, still likely >12 months away from CFBE

💰 C$1.7B, down C$254M from ~C$2.0B at March 31, 2020

📰 PT: C$25.00/HOLD (Canaccord); C$38.00/BUY (Cowen); C$29.00 PT/HOLD (Cantor)

📈 up 4.5% (C$$31.95) after earnings

Other Highlights (deck)~15.5% market share in Canada; ~54% market share for beverages; 17.3% market share for rec. flower, 13.7% for value rec. flower

Continued launching Cannabis 2.0 products, launched Martha Stewart branded CBD gummies, expanded distribution of Storz & Bickell accessories in the US, increased BioSteel (CBD) sales upon the re-opening of a number of retailers, improved its ecommerce platform for This Works

Flat medical cannabis sales in Canada as registered medical patients continue to see modest declines

International medical sales declined by ~13% due to temporary packing/supply issues, and lower flower sales in Germany on slower growth and increased competition

Aurora (ACB) — Q1/21 (reported 11/9):

🤯 Believes it is still possible to reach its previously communicated goal of positive EBITDA next quarter (lending arrangements requirement as well)

💰 C$67.8M Net Revenue (48% GM), essentially flat from C$67.5M previous Q. 48% GM down 2% but still higher than peers

🔥 (C$57.9) EBITDA Loss, largely due to restructuring payments (contract and employee termination) costs of $47.4M

🩸 ($142.8M) cash burn, raised C$114M through ATM during Q

💰 C$250M. Currently Seeking another C$500M ATM and funding losses w/ equity issuance (unlike CGC/CRON, there isn’t a large Alcohol/Tobacco partner)

📰 PT: C$11.00 (up from C$8.50)/HOLD (Canaccord); C$16.00 (up from C$10.00)/HOLD (Cowen)

📈 up 2.5% (C$$16.00) after earnings, above updated Analyst outlook

Other Highlights#1 medical market share in Canada

Reliva CBD maintains #1 market share among CBD products sold in brick-and-mortar retail (20,000+ doors) but still contributing just C$1.7M/Q in Revenue

Tilray (TLRY) — Q3/20 (reported 11/9):

🤯 7% GM, down from 31% Y/Y and increased from (11%) previous Q

💰 Revenue of $51.4M, flat Q/Q. Cannabis segment revenue actually down 11% to $314M, due to the discontinuation of bulk sales. Adult-use and International Medical sales grew 26% and 42%, respectively.

🔥 Adjusted EBITDA Loss narrowed to $(1.5M) compared to $(12.3M) Y/Y. Net Loss of $(2.3M) vs. $(81.7M) previous Q (cost cutting); expects EBITDA+ or BE next Q

🩸 Additional product launches (gummies, chocolates, beverages, and vape) should help EBITDA

💰 $155.2M cash with $209M remaining available though ATM

📰 $11.00 PT (down from $12.00)/HOLD (Cantor) / $8.50 PT/HOLD (Cowen)

📈 down 17.55% today (was up 7% after hours yesterday)

Other HighlightsTotal cannabis sold decreased 53% to 5,107kg from 10,848kg Y/Y (due almost entirely to the reduction of bulk sales)

Average cannabis net selling price per gram increased to $6.15 (C$8.15) compared to $3.25 (C$4.32) Y/Y and $2.64 (C$3.59) previous Q (continued shift in distribution channels and product mix — growth in International medical sales, a shift to higher potency and higher priced products in the adult-use market, and the continued growth of Cannabis 2.0 products)

Construction on the Company’s Portuguese cultivation facility remains largely on track (expects to spend less than original budget of ~$33M)

Cronos Group (CRON) — Q3/20 (reported 11/5):

🤯 4th consecutive Q of negative GMs. 🤯How? Sell ~24,000 kg of Cannabis for ~$51M but actually spend $56.5M to grow it.

💰 $11.4M in Revenue, up modestly from $9.9M Q/Q

🔥 EBITDA loss declined further to ($30.0M), down ($27.0M) Q/Q

🩸 $40M impairment against Lord Jones (CBD) last Q, Rev. down 27% to $1.6M

💰 $1.3B in cash

📰 PT: C$6.50 (SELL, Canaccord)

📈 Traded up 38% after 2 Days (Thursday/Friday)

Other Highlights (transcript)Market share in Canada recreational market significantly lags peers

Kurt Schmidt joined as President/CEO (Blue Buffalo, Gerber, Kraft Foods)

Launched medical cannabis brand (Peace Naturals) in pharmacies across Israel. Cronos Israel has been selling dried flower to the medical market and more recently launched oil. Launched Happy Dance (CBD skincare) w/ Kristen Bell

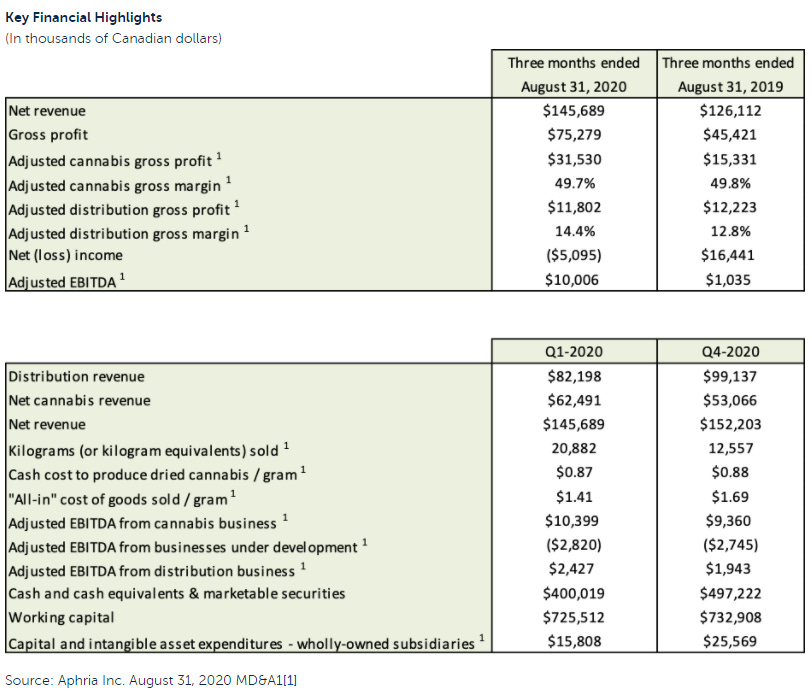

Aphria (APHA) — Q1/21 (reported 10/15):

🤯 Aphria does more Distribution revenue (56.4%) than Cannabis revenue (43.6%)

💰 Net revenue of C$145.7M (51.7% GM), down 4% from prior Q, solely due to lower distribution revenue. $69.6M in adult-use Cannabis though, an increase of 23% Q/Q.

🔥 EBITDA of $10M (7% EBITDA margin), up 17% from the prior Q (EBITDA from Cannabis business only up 11% from prior Q)

🩸 $250M cash ($50M stock) to be spent on SweetWater acquisition

💰 C$400M in cash (C$54M to be used for SweetWater)

📰 PT: C$11.75 (Cantor) / C$9.00 (AGP) / C$10.00 (Canaccord)

📈 Traded down 18% after earnings

Other Highlights#1 LP in adult-use (Canada) and continues to outgrow the industry. #1 or #2 positions across all major formats, with ~25% share in vapes, according to Hifyre

Push into value/larger pack sizes to target previously unserved customer segment

Have you looked into VALENS?