🤝 Cresco Labs acquires Columbia Care for $2.0B (~35% of pro forma company)

$1.4B+ in combined revenues (65% from retail), 130 dispensaries across 18 states. #1 market share in IL, PA, CO, VA; #2 in MA; path to Top-3 in NY, NJ, FL.

Press Release

Investor Presentation

Cresco Labs (CSE:CL) (OTCQX:CRLBF) and Columbia Care (NEO:CCHW) (CSE:CCHW) (OTCQX:CCHWF) announced today they have entered into a definitive arrangement agreement pursuant to which Cresco Labs will acquire all of the issued and outstanding shares of Columbia Care. Subject to customary closing conditions and necessary regulatory approvals, the Transaction is expected to close in Q4 2022.

🤝 Transaction Overview

Under the terms of the Arrangement Agreement, shareholders of Columbia Care will receive 0.5579 of a subordinate voting share of Cresco Labs for each Columbia Care common share (or equivalent) held, subject to adjustment representing total consideration enterprise value of ~$2.0 billion based on the closing price of Cresco Labs Shares on the CSE as of March 22, 2022. The Transaction provides Columbia Care Shareholders with premiums of ~16% based on the closing prices of the Columbia Care Shares and the Cresco Labs Shares, and (ii) 19%, based on the 20-day volume weighted average prices (VWAP) of the Columbia Care Shares and the Cresco Labs Shares, each on the CSE as of March 22, 2022.

💨 Superior Market Access

Largest Multi-State-Operator (MSO) by pro-forma revenue. Gives Cresco Labs the largest pro-forma revenue in cannabis today at over $1.4 billion

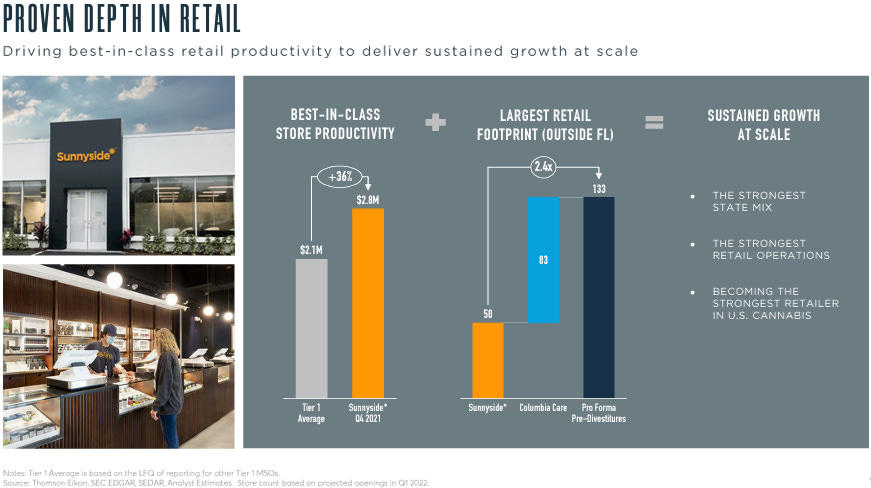

Strategic, national footprint. Over 130 retail stores across an 18 market footprint, representing the #2 retail footprint in the industry, and the #1 retail footprint outside of Florida. The combined company will cover all 10 of BDSA’s top-10 largest and fastest growing markets by 2025, representing ~55% of the U.S. population and over 70% of addressable cannabis market

Market share leader in key states. Independently, the companies currently have #1 share positions in four markets (IL, PA, CO, VA,), #2 share in MA, and a pathway to a top-3 position in three more (NY, NJ and FL), bringing the combined company to a material market position in seven of the top 10 markets by revenue in 2025, according to BDSA

Exposure to adult-use upside. Meaningful presence in today’s most influential markets and those with the biggest tailwinds for growth and adult use upside including: NY, NJ, VA, PA, OH, MD, and FL

🚚🏪 Proven Capabilities in Wholesale and Retail

The industry’s leading brand portfolio. #1 market share in the U.S. with strength in every major segment: #1 in branded flower, #1 in concentrates, #1 in vapes and top 5 in edibles, per BDSA

Most productive retail banner. Cresco Labs’ Sunnyside retail stores have average annualized revenue per store of over $11 million, the highest of any scaled national operator in the industry

Industry leading wholesale platform. Pro-forma Q4 2021 wholesale revenue of over $120 million, the highest in the industry

⚖️ Balanced Economics

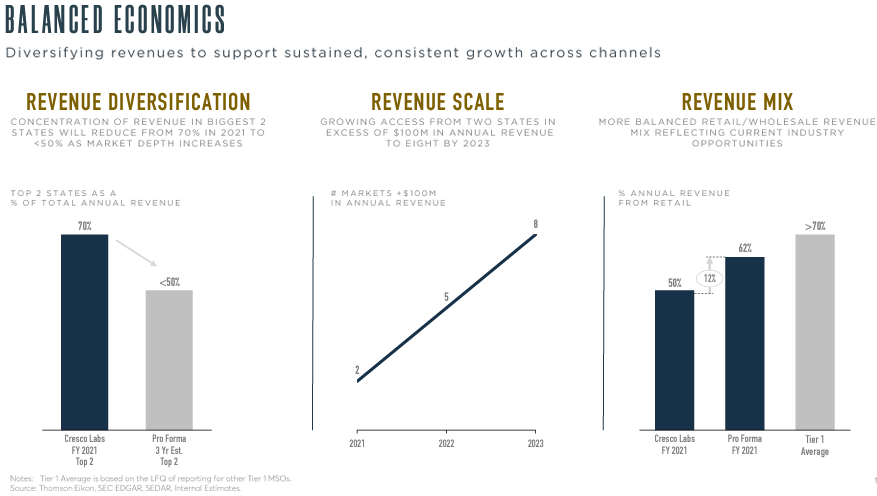

Increased scale and diversification. On a pro-forma basis, the Company expects to have $100M+ annual revenues in 8 different states by 2023 from going deeper across other markets and diversifying its revenue base

Improved revenue mix. Increased retail revenue mix to 65% of total, from 47% today (for Cresco standalone), increasing vertical integration and scale to drive profitability improvement

Opportunity for synergies and de-levering. Ability to increase retail productivity, reduce redundant operational and capital expenses as well as de-lever the organization ($400M Senior Secured Term Loan) through the proceeds from the sale of redundant licenses (NY, IL) and assets in high-value markets

🗒️ Notes:

Ability to Improve Net Debt ($224M Cash, $377M Debt) / Interest Rates. The company had $224M of cash and cash equivalents and $377M of Senior Secured Term Loan, net of discount and issuance costs. Proceeds from the sale of NY and IL licenses will go towards paying down debt, increasing cash for CapEx. Also the combined company should be able to lower its cost of debt (9.5% on $400M Senior Loan in August 2021) to levels comparable with Curaleaf (raised $425M at 8.0% in December 2021) and Trulieve ($350M at 8.0% in October 2021).

~16% premium for Columbia Care Seems Low. According to a BCG report in 2019, The long-term average premium for M&A from 1990–2018 was 30.6%, although conditions are very different today with COVID, the ongoing Russian invasion of Ukraine, and challenges of operating/being a publicly-traded Company in the Cannabis Industry.

Edibles Acquisition? Cresco Labs highlighted its leading market share position (#1 in four markets (IL, PA, CO, VA,), #2 share in MA, and a pathway to a top-3 position in three more (NY, NJ and FL). One place where it didn’t mention at #1 or top-3 position? Edibles, where the Company is top 5. Canopy has already tied up Wana, so if the company doesn’t go the organic route with its Mindy’s Edibles brand, it could look to Kiva (which it currently partners with for IL), Wyld, or Sunderstorm.

👋 Highly Objective is curated by Dai Truong, who leads Cannabis Investment Banking at Arlington Capital Advisors. Third-party information presented here and links to third-party content are for informational purposes only and are not intended as a recommendation, offer or solicitation for the purchase or sale of any financial instrument, security or investment. The information provided is not warranted as to completeness or accuracy and is subject to change without notice. Linking to third-party sites in no way implies an endorsement or affiliation of any kind between Arlington Capital Advisors, LLC, or its affiliates and any third party. The information in this blog constitutes my own opinions (and any opinions posted by guest bloggers from time to time) and it should not be regarded as a description of services provided by Arlington Capital Advisors, LLC or any affiliate.